Takeaways from Thomson Reuters Report: FinTech, RegTech, and the role of compliance in 2023

We know you’ve been paying attention to FinTech news. It comes as no surprise that FinTech, or financial tech, and RegTech, or regulatory tech, have experienced a rapid growth rate in the last couple of years. In turn, this has led to changes in our regulatory environment. Read on for a quick and dirty recap on the state of FinTech, RegTech, and compliance in 2023.

We’re summarizing and referencing The Thomson Reuters Report on FinTech, RegTech, and the role of compliance in 2023. This report explores the current state of the industry, its challenges, and opportunities and predicts what the future will look like.

Let’s get into it.

What’s going on? High-level takeaways

We read the tiny print in the report, so you don’t have to. Here are the points you need to know (plus some great graphs!)

Diverse use for FinTech and RegTech applications

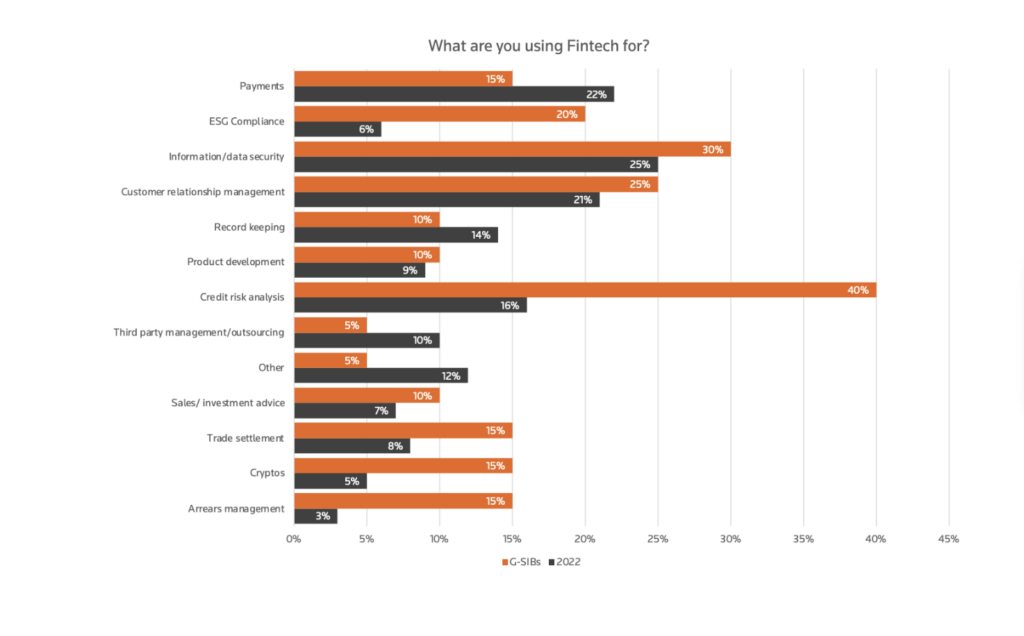

40% of global banks (the important ones, called G-SIB) were using FinTech applications for information security, whereas 30% of total respondents used FinTech. Half of the respondents fully or partially implemented a RegTech solution in 2022, up from 38% the year prior.

A slowdown in FinTech (except for you, UK)

According to Innovate Finance’s 2022 Summer Investment report, in the first half of 2022, FinTech investment worldwide reached $59 billion.

With 3,045 deals completed, this was flat year-over-year.

An exception to the slowdown was in the UK FinTech sector, with investment reaching $9.1 billion – a 24% year-over-year increase from the first half of 2021. The UK is second in FinTech investment, behind the United States.

People aren’t as excited as before

For FinTech overall, this year’s survey reported that 15% of respondents were extremely positive, compared with 31% last year. There was an increase in positive feelings (61%) compared to 2021 (51%).

For RegTech, 15% of respondents felt extremely positive compared with 26% in 2021. There was an uplift in those who felt mostly positive — 63% — compared with 48% in 2021.

But there is still a need to help meet increasingly challenging regulations

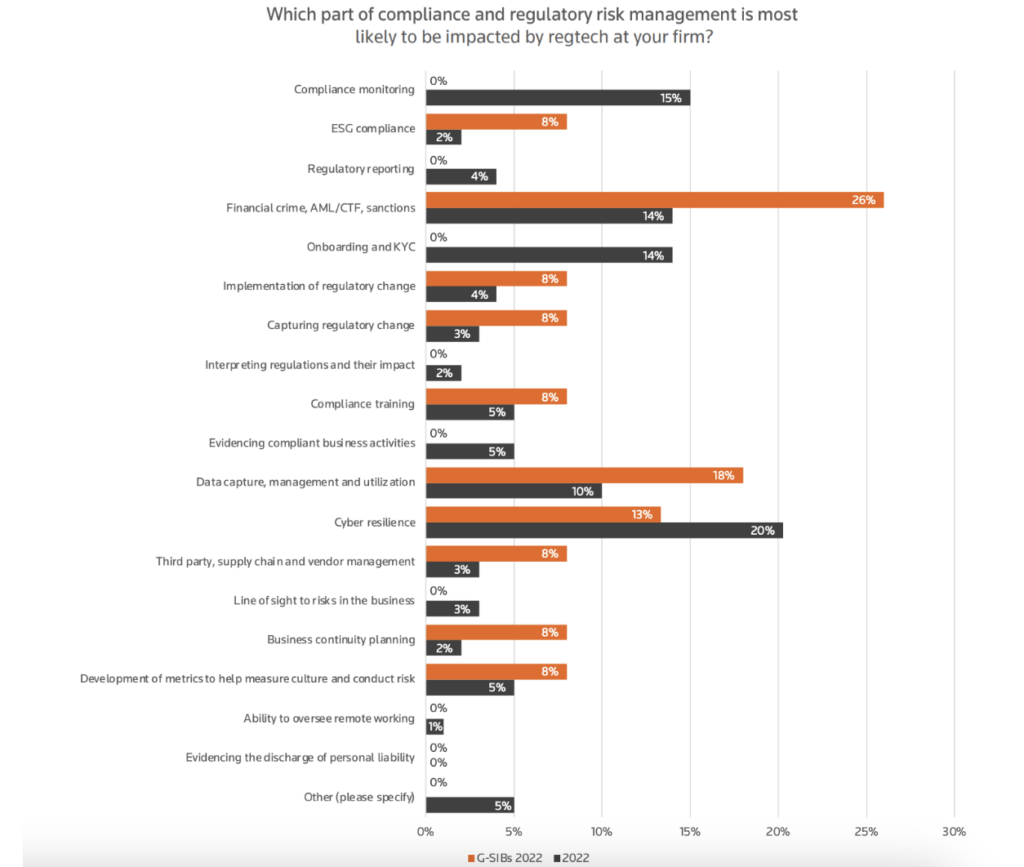

This year’s survey highlighted financial crime as the most impactful area for RegTech applications. No doubt partly to aid firms in their compliance efforts regarding sanctions following Russia’s invasion of Ukraine.

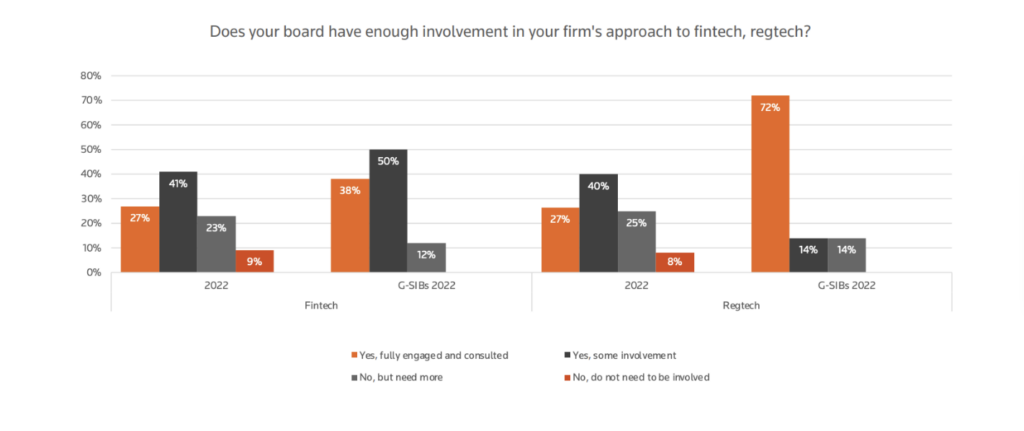

Interestingly, firms are in need of more oversight and involvement from their boards when implementing and executing tasks related to FinTech and regtech. There was a significant uptick in boards involved in RegTech year-over-year. And, all together now, we say, “YES!”

In RegTech to the greater regulatory risk, the survey reported significant challenges when using FinTech and RegTech applications.

Implementation challenges

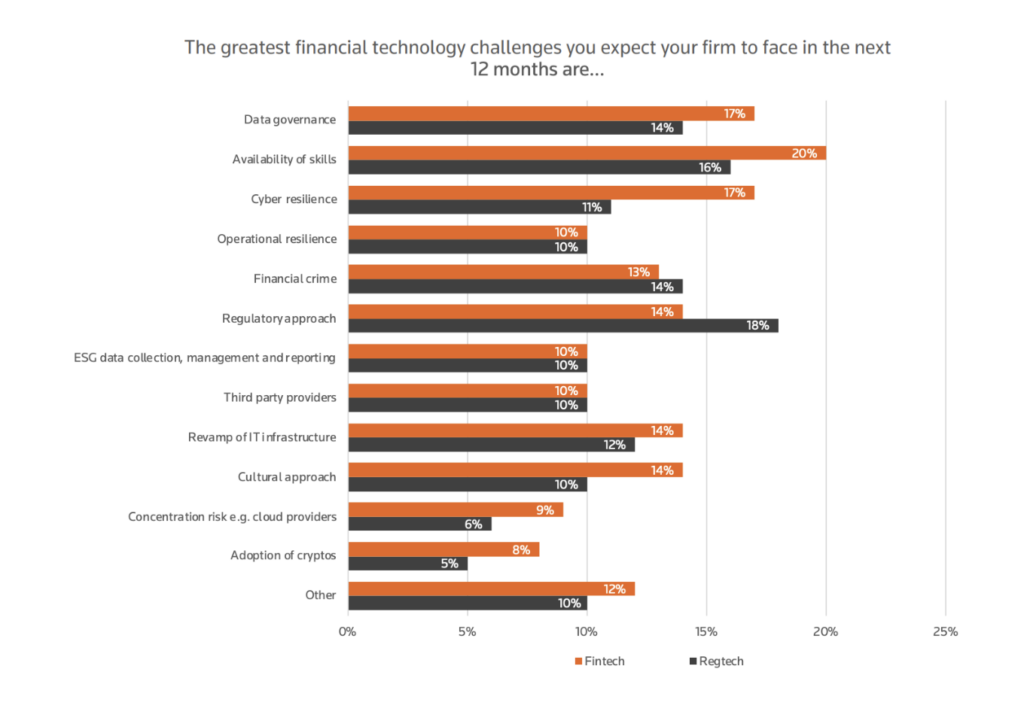

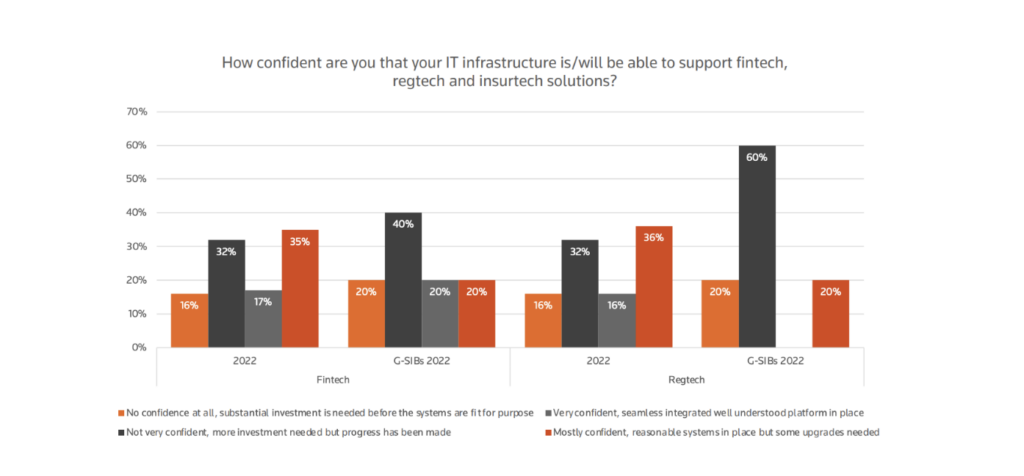

Reasons given for not implementing FinTech included a lack of investment, lack of in-house skills, and poor infrastructure. This mirrors some of the wider challenges that respondents identified when deploying FinTech applications, where the availability of skills, data governance, and the regulatory approach featured prominently.

Existing IT infrastructures have been challenged to support future FinTech and RegTech solutions, and this year’s results were no exception.

Regulators need tech help too

Regulators are also adopting technological solutions to help with their supervisory roles and with the management of enormous quantities of data. The pandemic accelerated the use and adoption of technological solutions (And… goodbye Silicon Valley Bank. Now we’ve seen what happens in the wake of an event like this)

Regulators have themselves adopted solutions to meet evolving supervisory approaches, including the need to gather and analyze increasingly large volumes of data.

This bleeds into a nice factoid about implementing these types of tech: businesses need to diversify the skillsets of their boards and risk and compliance functions to be able to meet the tech need. Firms in the United States are ahead of peers, with 38% widening skill sets within the risk and compliance functions and investing in specialist skills.

Back to my main point: RegTech solutions are walking regulators into the light of technology. While we’re not at an inflection point–more regulators using tech vs. not using tech–we are seeing a growing number of respondents report that the way they execute their jobs is in consideration of RegTech.

Looking forward

The FinTech and RegTech industry is still a significant growth market, but companies must innovate to stay ahead of the competition. Compliance will continue to be a crucial factor, and RegTech solutions will become more prevalent. Collaboration between FinTech and traditional financial institutions presents new opportunities for growth and innovation.

Regulations will continue to evolve, and companies must keep up with the changes to avoid costly fines and legal penalties. AI and blockchain technology will play a more significant role in the industry, providing greater efficiency, transparency, and security.

Firms should therefore continue to consider investment in technology, and in the supporting IT infrastructure and associated skillsets, although any such investment needs careful planning.

Firms need to be certain that FinTech and RegTech will deliver the stated benefits. A well-resourced, highly skilled compliance function will be invaluable in successfully navigating the optimal use of digital solutions.

Bank of England and the UK Financial Conduct Authority

Ready to use compliance as an advantage?

Compliance is the foundation a company needs to build its reputation, signaling that it’s operating ethically with the safety of its users and stakeholders in mind. At Thoropass, we help you get and stay compliant with our all-in-one compliance solution that streamlines automation, offers unparalleled support from experts, and provides a seamless audit experience. Talk to an expert today to learn more.

Related Posts

Stay connected

Subscribe to receive new blog articles and updates from Thoropass in your inbox.

Want to join our team?

Help Thoropass ensure that compliance never gets in the way of innovation.

.png)